The Global Pension Crisis: A Ticking Time Bomb in Plain Sight

Across the developed world, a quiet but relentless mathematical equation is falling apart. It’s the simple arithmetic that underpins the very promise of retirement—the promise that after a lifetime of work, society will provide a measure of comfort and security. This promise, one of the great social contracts of the 20th century, is now under threat.

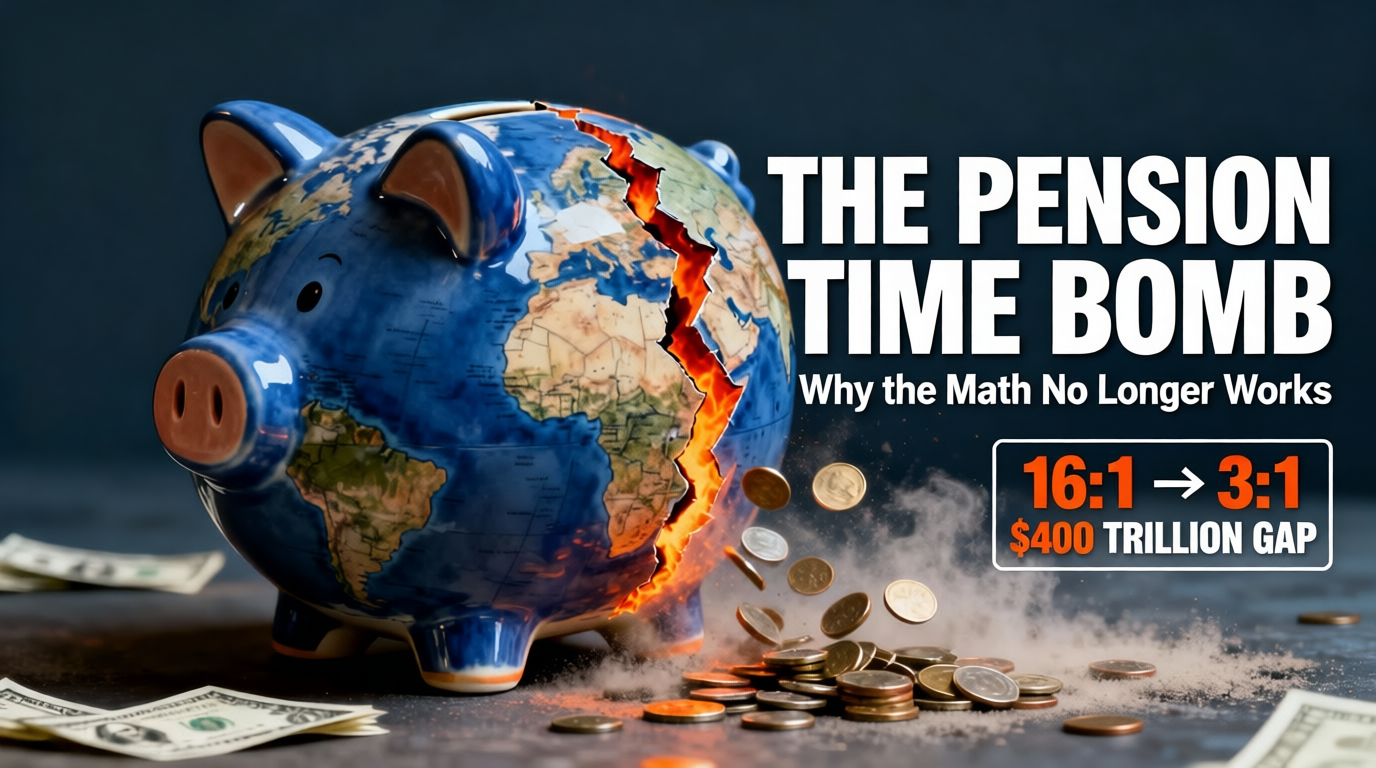

The numbers are stark and speak a universal language of demographic decline. In the 1950s, the United States had a robust base of 16 workers for every single retiree. Today, that number has collapsed to fewer than three. And by comparison, the U.S. is still in a relatively enviable position. Look to Japan, where the working-age population has shrunk by a staggering 14 million people since 1995. Or consider France, where pension spending already consumes 14% of the country’s entire economic output, one of the highest shares in the world.

These systems were built for a different era—a world where people had more children and spent fewer years in retirement. But that world is gone. Global life expectancy has jumped by an incredible 30 years over the past century, while birth rates have collapsed below replacement levels in nearly every developed nation. The numbers, quite simply, no longer balance.

By 2050, one in six people on Earth will be over the age of 65, a significant increase from one in eleven today. This silver tsunami coincides with a drought of new workers. Fewer babies born today mean fewer taxpayers entering the workforce tomorrow to support the ever-growing number of retirees. The foundation of the modern pension system is cracking.

Yet, despite the glaring red flags, a profound political paralysis has set in. Fixing the pension problem invariably means asking citizens to accept one of three bitter pills: work longer, pay more in taxes, or receive less in benefits. None of these options wins elections. Consequently, governments are kicking the can down the road, a short-term strategy that is already destabilizing major economies. By the numbers alone, the situation is only going to get worse.

So, the critical questions remain: Is the pension problem solvable? What happens if we continue to ignore it? And is there any country that has found a path through this demographic quagmire?

The Broken Promise: How the 20th Century Model Became Obsolete

Pensions were one of the greatest economic promises of the 20th century. The deal was straightforward: you work hard now, you contribute a portion of your earnings to the system, and then, upon retirement, society takes care of you. It was a powerful social compact that provided dignity and security for millions.

But that deal only works if the underlying math holds, and increasingly, it doesn’t. The vast majority of public pension systems around the world operate on a “pay-as-you-go” (PAYG) model. The money you pay in taxes today doesn’t go into a personal vault with your name on it, earmarked for your future. Instead, it goes straight out the door to fund the benefits of today’s retirees. Your own retirement, in turn, is intended to be funded by the next generation of workers.

This system worked brilliantly in the decades following World War II. Economies were booming, birth rates were high, and the demographic pyramid was wide at the bottom, with a massive base of workers supporting a relatively small number of people collecting benefits. The United States’ ratio of 16 workers per retiree in 1950 is a perfect illustration of this golden age.

Fast forward to today, and that ratio has collapsed to just 2.7 workers per retiree. This dramatic shift is even more profound than it appears, as it includes the massive influx of women into the workforce since the mid-20th century—a one-time demographic boost that cannot be repeated. Projections suggest this ratio will fall further to 2.3 by 2035. This trend is a global phenomenon. Across Europe, Japan, and South Korea, the ratios are even more dire, with some nations already approaching a mere two workers for every retiree.

This is what economists call a “dependency ratio crisis.” It’s a simple, brutal equation: too few people are working and paying into the system to support too many people who are not.

The American Dilemma: The Looming Threat of Insolvency

In the United States, the most immediate danger is the insolvency of the Social Security system. The U.S. runs the largest pension system in the world, with over 73 million recipients. It is funded by a 12.4% payroll tax, split evenly between employees and employers. In theory, this should be self-balancing; as long as enough people are paying in, there should always be enough to pay out.

But that balance is now fundamentally broken. The Social Security Administration itself projects that the program’s combined trust funds will be depleted by 2035. After that point, ongoing payroll taxes will only be sufficient to cover about 83% of promised benefits. This isn’t a speculative fear; it’s a official forecast. In practical terms, unless Congress acts, retirees could face an automatic 17% cut to their monthly income.

For the average American retiree living on a fixed income of around $1,900 a month, that translates to a loss of over $300 they simply cannot afford. This calculation doesn’t even account for the silent thief of inflation, which relentlessly erodes the purchasing power of every dollar, making each Social Security check worth less in real terms with every passing year.

The crisis isn’t confined to the federal level. State-level public pension funds are in even deeper trouble. As of 2022, state pensions across the U.S. were underfunded by a staggering $1.27 trillion. In states like Illinois, New Jersey, and Kentucky, public pension plans have less than 60% of the assets needed to meet their future obligations. This shortfall represents a massive future liability that will inevitably compete with funding for schools, infrastructure, and public safety.

Japan’s Perfect Storm: Running Out of People

If America’s primary problem is running out of money, Japan’s is running out of people. Japan faces a demographic challenge on a scale unmatched by any other major economy. With a median age of nearly 50, it has one of the oldest populations on the planet. By 2050, close to 40% of Japanese citizens will be over 65. Since 1995, its working-age population has shrunk by 13 million people—a number larger than the entire population of Greece.

This demographic collapse means pension spending now consumes over 9% of Japan’s GDP. But beyond the simple math of an aging society, Japan shoulders a unique and tragic burden: a “lost generation” that never had a fair shot at saving for retirement.

After Japan’s asset price bubble burst in the early 1990s, the country entered a period of prolonged economic stagnation known as the “Lost Decades.” Companies froze hiring and slashed wages, creating an “Employment Ice Age.” Millions of young graduates found themselves locked out of the traditional lifetime employment tracks and were forced into part-time or temporary contract work, known as haken or freeter.

These jobs came without benefits, without job security, and, most critically, without stable access to the corporate pension system. Now, 30 years later, this generation is entering its 40s and 50s with scant savings, patchy pension contributions, and no stable safety net. Economists warn that when they reach retirement age, Japan could face a devastating social crisis: millions of elderly citizens with almost no pension income at all.

To support its aging population, the Japanese government has been forced to borrow heavily. Public debt now exceeds 250% of its GDP, the highest ratio in the developed world. The nation is caught in a vicious cycle: it must borrow to pay for today’s pensions, placing an ever-heavier burden on a shrinking pool of future taxpayers.

The French and Chinese Challenges: Fiscal Weight and Demographic Speed

France presents a different facet of the crisis. Its problem is not immediate insolvency, but the sheer fiscal weight that pensions place on the national budget. With pension spending eating up 14% of GDP, every euro directed to retirees is a euro that cannot be invested in hospitals, renewable energy, defense, or education. This creates a fierce competition for public funds, stifling investment in the country’s future.

This fiscal pressure is precisely why the French government attempted to raise the retirement age from 62 to 64 in 2023. The move triggered massive nationwide strikes, with garbage piling up on the streets of Paris and transport networks grinding to a halt. For the French public, the right to retire at 62 is a hard-won social benefit, and any attempt to curtail it is seen as a fundamental betrayal. The political firestorm that followed saw President Macron’s approval ratings plummet, a clear warning to any leader considering similar reforms.

Then there is China, a case study in demographic whiplash. Unlike Japan or France, China’s pension system is relatively new, but the country is aging at a record-breaking speed. Decades of the One-Child Policy have left it with a distorted population structure: a narrow base of young workers supporting a rapidly bulging cohort of elderly citizens. By 2050, nearly 366 million Chinese will be over the age of 65—more than the current total population of the United States.

According to government forecasts, China’s national pension fund could run dry by the early 2030s. This poses an existential challenge for a country whose citizens have become accustomed to steadily rising living standards. Unlike advanced Western economies, China has not had decades of prosperity to build up substantial private savings. Millions of retirees will depend almost entirely on a public system that may not be there when they need it most, creating a potent source of social unrest.

The Political Paradox: Why Solutions Are So Elusive

Add these national crises together, and the global picture looks grim. The World Economic Forum estimates that by 2050, there will be a $400 trillion gap between what people need in retirement and what has actually been saved. This figure is about four times the size of the entire global economy today.

If the problem is so obvious, what is being done to fix it? The unfortunate answer, in most places, is very little.

The core of the issue is a fundamental mismatch of time horizons. In democracies, political leaders typically think in two-to-five-year cycles, focused on the next election. Pension systems, by contrast, are 100-year promises. Solving the pension crisis requires imposing short-term pain for long-term gain, a trade-off for which politicians are rarely rewarded.

This is why even ideological opponents often find strange agreement on this topic. In the U.S., both Donald Trump and Joe Biden have repeatedly pledged not to touch Social Security benefits. The political calculus is simple: the coalition of older voters is among the most reliable at the ballot box, and they have the most to lose from any reform.

When governments do muster the courage to act, they are generally left with three unappealing options, each with significant downsides:

- Raising the Retirement Age: Economically, this is a logical response to increasing lifespans. But as France demonstrated, it is politically explosive, perceived as stealing hard-earned leisure years from workers.

- Cutting Benefits: While it balances the books on paper, reducing payouts risks pushing millions of seniors into poverty. In Japan, one in five seniors already lives in relative poverty; further cuts could be catastrophic.

- Raising Taxes: Increasing payroll taxes to bolster revenue places the burden squarely on younger workers, a generation already straining under the weight of student debt, soaring housing costs, and inflation. This can foster resentment and a sense of intergenerational injustice, leading younger, mobile workers to seek opportunities elsewhere.

The Privatization Experiment: Lessons from Chile

Faced with the limitations of public systems, some countries have experimented with privatization. The most famous case is Chile, which in 1981 replaced its state-run pension system with a model based on privately managed individual retirement accounts.

For a time, the Chilean model was hailed as an international success story. It inspired reforms across Latin America and Eastern Europe. The theory was sound: shift responsibility from the government to the individual, reduce long-term strain on public finances, and harness the power of market investments to grow savings.

But over time, significant cracks appeared. Many low-income workers could not afford to contribute consistently. Market downturns wiped out returns for those nearing retirement. The result was that for a large segment of the population, the privatized pensions were far smaller than promised. The people of Chile took to the streets in protest, demanding reform. The government was eventually forced to step back in, guaranteeing minimum payments and effectively re-socializing the system it had once privatized. The lesson was clear: pure privatization carries high risks of leaving vulnerable populations behind.

Glimmers of Hope: Models for Sustainable Reform

Despite the daunting challenges, a handful of countries are demonstrating that sustainable reform is possible. They offer valuable blueprints for others to follow, emphasizing gradual, automatic, and transparent adjustments.

The Australian Model: Mandatory Savings

Australia’s “Superannuation Guarantee,” often called “super,” is a mandatory retirement savings system integrated into the workplace. Employers are required by law to contribute a percentage of an employee’s earnings (currently 11%) into a private, personal investment account. Employees can also make voluntary contributions, with both streams receiving favorable tax treatment.

Over decades, these contributions are invested in diversified portfolios, growing into a substantial nest egg that supplements or even replaces the government pension. The system has been running for over three decades and has amassed over $4 trillion in assets—a pool larger than Australia’s entire annual GDP.

However, it is not a perfect solution. The generous tax breaks primarily benefit higher-income earners who can afford to contribute more. Meanwhile, lower-income workers, who benefit less from tax incentives, may still rely heavily on the public pension. While it reduces long-term public liability, it does so at the cost of significant government revenue foregone.

The Danish and Dutch Model: The Automatic Adjuster

Denmark has implemented one of the most elegant solutions to the political problem of raising the retirement age. Instead of a fixed number, the official retirement age is automatically linked to increases in national life expectancy. There is no political battle every few years; the adjustment is built into the system.

When this rule was introduced in 2006, the retirement age was 65. It is scheduled to rise to 68 by 2030 and could reach 70 by the 2040s. This gives citizens decades of advance notice to plan their careers and savings, ensuring the system remains solvent without the shock of sudden, politically-driven reform. Germany and the Netherlands have adopted similar models, tying their pension ages to demographic data.

The Swedish Model: Notional Defined Contributions

Many economists point to Sweden as the gold standard for pension reform. In the 1990s, facing a collapsing pay-as-you-go system, Sweden undertook a radical overhaul. It moved to a “notional defined contribution” (NDC) system.

Here’s how it works: contributions from workers are still used to pay current retirees, but each individual’s account is credited with “notional” contributions that track their lifetime payments. The critical innovation is that the ultimate payouts are automatically adjusted based on the economy’s health and life expectancy. When the Global Financial Crisis hit in 2008, for example, Swedish pension benefits were automatically adjusted downward by about 4%. The system remained solvent, and because the rules were transparent and applied to everyone equally, there was no public outrage or panic. The system corrects itself, distributing the demographic and economic pain fairly and predictably.

Targeted Support: Means Testing and Flat Pensions

Other countries are using targeted approaches to ensure limited resources go to those who need them most.

- Australia and Canada employ means testing for their public pensions. Retirees with high incomes or substantial private assets see their government pension reduced or phased out entirely.

- New Zealand uses a different, simpler approach. Everyone over 65 receives a universal flat-rate pension, which is then taxed as regular income. This means wealthier retirees, who are in a higher tax bracket, effectively pay a larger portion of their pension back to the government. It’s a transparent way to target support while maintaining the principle of universal eligibility.

Conclusion: The High Cost of Inaction

The global pension crisis is not a surprise. It is a slow-motion event, predicted by demographers for decades. The countries navigating it most successfully are those that acted early, implementing gradual, automatic, and transparent reforms. They have shown that it is possible to preserve the social contract of retirement without bankrupting the state.

The key lesson is that trust is paramount. Citizens need to believe that the system will be there for them, that the rules won’t change capriciously, and that contributing today will yield a secure tomorrow.

The alternative to thoughtful reform is not the preservation of the status quo, but a sudden and chaotic reckoning. If economics teaches us anything, it is that the longer you ignore a predictable problem, the more catastrophic and painful the eventual solution becomes. The ticking of the demographic clock is growing louder. The question is whether our political systems are capable of listening before time runs out.